Most small business owners assume their general liability policy has them covered if something goes wrong online. It doesn't. Standard business insurance excludes digital risks entirely, which means a ransomware attack or data breach could leave you with six-figure losses and no financial safety net. Understanding what is cyber liability insurance, what it actually covers, and whether your business needs it is one of the most practical things you can do to protect what you've built.

Table of Contents

- Key takeaways

- What is cyber liability insurance?

- What cyber liability actually covers

- How cyber liability insurance works: claims and pitfalls

- Is your business ready for cyber coverage?

- How to get covered and integrate it into your risk plan

- My honest take on cyber liability insurance for SMBs

- How Ventisconsulting can help protect your business

- FAQ

Key takeaways

| Point | Details |

|---|---|

| General insurance won't cover you | Standard liability and property policies exclude cyber events, leaving a significant gap. |

| Two coverage types matter | First-party coverage handles your direct losses; third-party coverage addresses lawsuits and regulatory fines. |

| Cost is more accessible than you think | Average annual premiums for small businesses run around $1,740. |

| Security controls affect your coverage | Failing to implement required controls like multi-factor authentication can get your claim denied. |

| Insurance is one part of a larger strategy | Cyber liability insurance works best when paired with strong IT security practices, not as a standalone fix. |

What is cyber liability insurance?

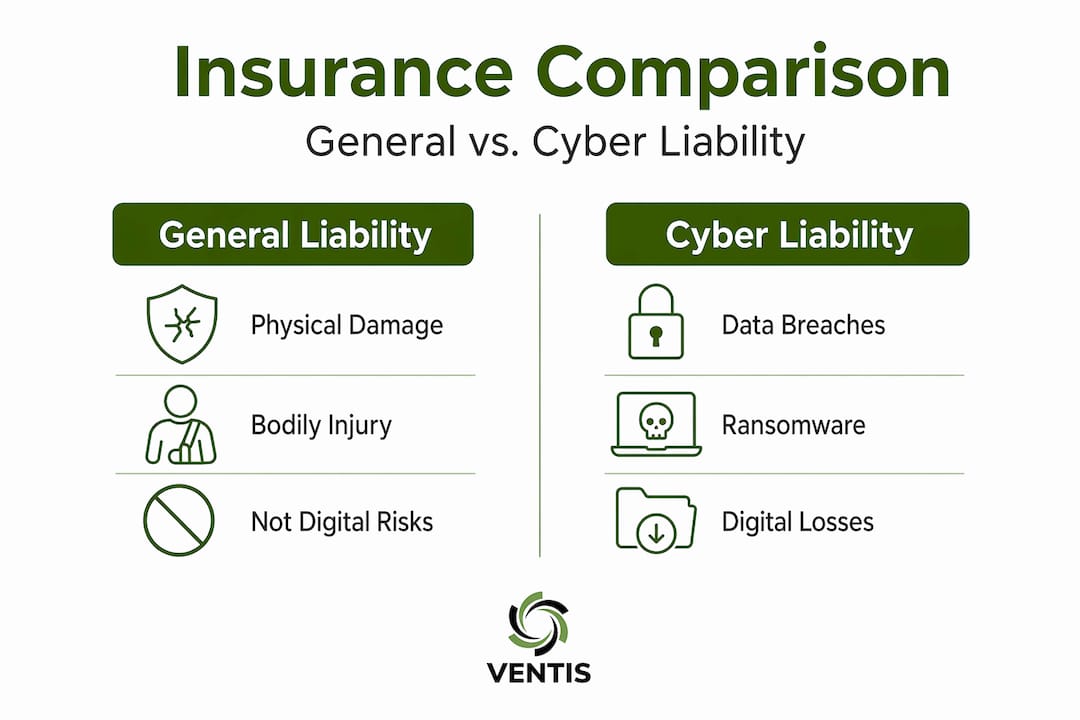

Cyber liability insurance is a specialized policy designed to cover financial losses that result from digital threats. Think of it as the gap filler between your existing business insurance and the reality of operating in a connected world. A fire damages your physical office? Your property insurance responds. A hacker steals your customer data? That same property policy won't pay a cent.

Policies are structured into two distinct categories:

- First-party coverage pays for your direct losses. This includes costs to investigate a breach, restore lost data, notify affected customers, and recover from a ransomware attack.

- Third-party coverage pays when others sue you or regulators fine you because of a breach. If a customer's personal data is exposed and they take legal action, this is the coverage that responds.

Here's a quick comparison to clarify how cyber liability fits alongside your existing policies:

| Policy type | What it covers | What it misses |

|---|---|---|

| General liability | Bodily injury, property damage, advertising injury | Cyber events, data theft, digital asset loss |

| Property insurance | Physical damage to buildings and equipment | Software, data, and digital infrastructure |

| Cyber liability insurance | Data breaches, ransomware, business interruption, legal costs | Intentional acts, certain exclusions (see below) |

A common misconception is that cyber coverage is only for large companies storing thousands of credit card numbers. The reality is that any business using email, storing client information, or relying on software to operate faces genuine cyber exposure. That's most businesses in Pittsburgh and across the country.

What cyber liability actually covers

Cyber risk coverage goes well beyond just data breaches. Modern policies are built to reflect how attacks actually unfold and what they actually cost.

On the first-party side, a typical policy covers:

- Ransomware response: Forensic investigation, system recovery, and in some cases, the ransom itself. The median ransom paid in 2024 was $115,000, though 64% of victims refused to pay by relying on backups.

- Data restoration: The cost to rebuild or recover lost or corrupted data.

- Business interruption: Revenue lost while your systems are down following a covered event.

- Notification costs: Legally required notifications to affected customers and credit monitoring services.

On the third-party side, you get protection from:

- Lawsuits filed by customers, vendors, or partners whose data was compromised

- Legal defense costs and settlements

- Regulatory fines and penalties for non-compliance with data protection laws

What makes modern cyber insurance explained well is that many leading insurers now go beyond simply paying claims. Pre-loss services like vulnerability assessments and 24/7 breach coaches are built into better policies, meaning you get expert support the moment an incident starts, not after you've already made costly mistakes.

Pro Tip: Ask any insurer you're considering whether their policy includes access to a breach coach. Having an expert on call the moment you discover an attack can drastically reduce your total incident costs.

The benefits of cyber liability insurance extend further when you consider compliance. Cyber insurance is becoming essential for regulatory compliance as data protection laws tighten and litigation costs climb. If your industry handles sensitive personal or financial data, carrying coverage may not be optional for much longer.

How cyber liability insurance works: claims and pitfalls

Understanding how cyber liability works in practice means knowing what happens after an incident and what could prevent you from collecting.

Here's how a typical claim process unfolds:

- Incident discovery: You identify a breach, ransomware infection, or system compromise.

- Immediate notification: Contact your insurer right away. Many policies require prompt notification, and delay can be grounds for denial.

- Approved vendor activation: Your insurer typically has a panel of approved forensic and legal vendors. Using outside help without authorization can reduce or void your payout.

- Technical assessment: The insurer's team evaluates the scope of the incident and activates the appropriate coverage components.

- Recovery and settlement: Costs are covered according to policy terms, and any third-party claims are managed through your legal coverage.

Misunderstanding business interruption triggers is one of the most expensive mistakes small business owners make. Business interruption coverage typically requires a direct causal link between the cyber event and the revenue loss, and the definition of that link varies by policy.

Common exclusions you need to know about include:

- Negligence, employee misconduct, and social engineering attacks (though riders can add social engineering coverage)

- Acts of war or nation-state attacks

- Pre-existing vulnerabilities that were known and unaddressed

The requirement that catches most small businesses off guard is security control compliance. Insurers require controls like multi-factor authentication as a condition of coverage. If you don't have MFA enabled and you get breached, your claim could be denied outright. This is not a technicality buried in fine print. It is a hard policy condition.

"Cyber insurance claims often arise from human error, system outages without data compromise, and social engineering losses. Not just the dramatic breaches you read about in the news." — Source: Insurance Business

Understanding social engineering defense is particularly relevant here, since many claims stem from employees being deceived rather than systems being hacked.

Is your business ready for cyber coverage?

Before you buy a policy, it helps to understand what drives cost and whether the investment makes sense for your situation.

| Factor | How it affects your premium |

|---|---|

| Revenue and business size | Higher revenue usually means higher premiums |

| Industry type | Healthcare, finance, and retail face higher risk ratings |

| Data volume stored | More customer records means greater exposure |

| Security controls in place | Strong controls like MFA and endpoint protection reduce premiums |

| Claims history | Prior incidents raise your rates significantly |

The average annual cost of $1,740 is a reasonable baseline for small businesses, though coverage limits, industry, and existing security posture will push that number up or down. The real question isn't whether you can afford the premium. It's whether you could absorb a six-figure breach response on your own.

Your risk exposure is higher than you might think. Cyber claims arise from human error and system outages just as often as from sophisticated attacks. Any business with employees, email, and a network has exposure.

Pro Tip: Before shopping for coverage, pull together a basic inventory of the data you hold, the software you rely on, and any existing security controls. Insurers will ask for this information, and having it ready speeds up the application and often improves your pricing.

Reviewing your cybersecurity compliance practices before applying is worth the time. Insurers reward businesses that have taken proactive steps toward security, and it may directly reduce your premium.

How to get covered and integrate it into your risk plan

Getting cyber liability insurance isn't just about signing a policy. It works best when connected to your broader approach to IT security and incident response.

Here's what to focus on when getting started:

- Work with a specialized advisor. Cyber insurance advisors act as security translators between your IT team, leadership, and insurers. They can articulate your risk in financial terms and help you find coverage that actually fits.

- Ask the right questions before buying. Find out what security controls are required, whether social engineering is covered, what vendors you must use during a claim, and how business interruption is triggered.

- Pair coverage with strong IT security. Cyber insurance works alongside security controls to reduce both the likelihood and the financial impact of an incident. One without the other leaves real gaps.

- Understand your incident response plan. Know who to call first when something happens, whether that's your IT provider, your insurer, or both. Speed matters enormously in breach response.

- Review your policy annually. Cyber policies are evolving to reflect actual operational risks beyond data breaches. What covered your business two years ago may not match your current risk profile.

Connecting coverage to your SIEM and monitoring tools also strengthens your insurer relationship. Documented detection and response capabilities demonstrate that your business takes risk management seriously, and insurers price that accordingly.

My honest take on cyber liability insurance for SMBs

I've worked with a lot of small and mid-sized business owners in Pittsburgh who treat cyber insurance as an afterthought, something they'll get around to eventually. That mindset changes fast after an incident.

What I've learned is that the businesses that benefit most from cyber coverage are the ones that treat it as part of their risk management strategy, not a replacement for it. If you have weak security controls, a policy won't save you. You'll either get denied coverage outright or discover your claim falls into an exclusion you didn't read carefully enough.

The other thing worth saying plainly: why is cyber insurance important isn't just about covering losses. The pre-loss services embedded in better policies, breach coaches, vulnerability scans, and incident response coordination, are often worth the premium on their own. Having an expert in your corner the moment something goes wrong is a meaningful advantage for a small business that doesn't have an in-house security team.

My take is this. Get the coverage, but do the security work first. The two go together. And don't wait until renewal season to review your policy. The threat landscape shifts fast, and emerging AI-driven risks are creating exposures that older policies weren't written to address.

— Greg

How Ventisconsulting can help protect your business

If this article raised more questions than it answered, that's actually a good sign. It means you're thinking about your business's risk the right way.

Ventisconsulting works with small and mid-sized businesses across Pittsburgh to close the gap between their IT security posture and what insurers actually require. From managed IT services that keep your systems updated and monitored to security responsibility frameworks that align your controls with insurer expectations, we help you show up to your policy application with confidence. When your technology is managed properly, you reduce your premium exposure, avoid claim denials, and respond to incidents faster. Check out our managed IT solutions to see how we support businesses like yours.

FAQ

What does cyber liability insurance cover?

Cyber liability insurance covers direct losses from events like ransomware, data breaches, and system outages, as well as third-party costs including lawsuits, legal defense, and regulatory fines. Most policies also include breach response services such as forensic investigation and customer notification.

How much does cyber insurance cost for small businesses?

The average annual cost for small businesses is approximately $1,740, though premiums vary based on industry, revenue, data volume, and the strength of existing security controls.

Can my general liability insurance cover a cyberattack?

No. General liability and property insurance policies typically exclude cyber events and digital risks entirely, which is why a separate cyber liability policy is necessary.

What can cause a cyber insurance claim to be denied?

Claims are commonly denied when businesses fail to meet required security controls like multi-factor authentication, use unapproved vendors during incident response, or experience losses from excluded causes such as employee negligence or social engineering without a specific rider.

Do small businesses really need cyber liability insurance?

Yes. Most cyber claims stem from human error, system outages, and social engineering, not sophisticated attacks targeting large enterprises. Any business with employees, email access, and customer data carries real exposure that standard insurance does not address.